Don’t miss the long term opportunity for cloud providers

Wednesday 22 March 2023

Portfolio insights

The cyclical nature of enterprise cloud spend is a positive signal. It validates the flexible and scalable nature of cloud computing and thus its long term value to business users.

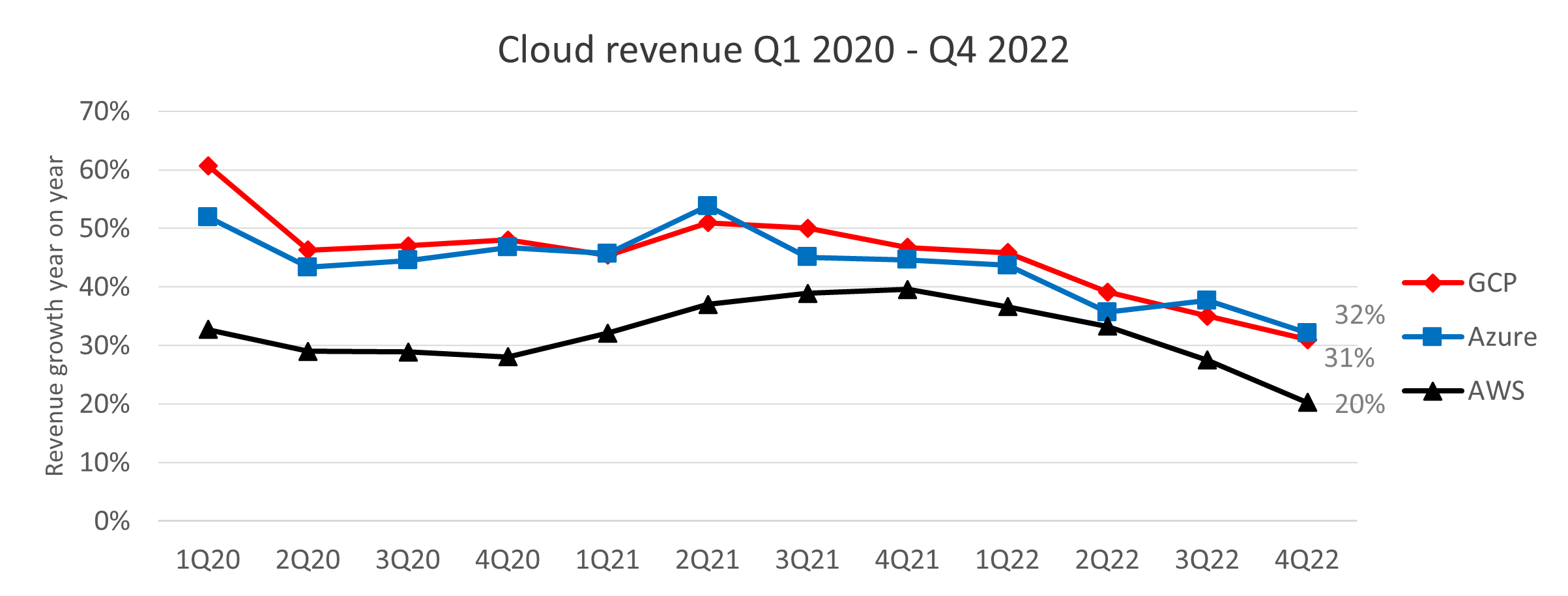

4Q22 results – slowing growth and cautious outlook

Q4 earnings from the largest public cloud providers show a gloomy year ahead for cloud spend.

Amazon

Amazon attributed slowing growth to macroeconomic uncertainty.

“We saw our year-over-year growth rates slow as enterprises of all sizes evaluated ways to optimise their cloud spending in response to the tough macroeconomic conditions.”

Management discussed some of the ways customers are optimising expenses:

- Switch to lower cost products

- Run calculations less frequently

- Adopt cheaper types of storage

And pointed to a foggy outlook:

“As we look ahead, we expect these [customer] optimisation efforts will continue to be a headwind to AWS growth in at least the next couple of quarters…”

This was echoed in similar comments from Microsoft and Google.

Microsoft

“Just as we saw customers accelerate their digital spend during the pandemic, we are now seeing them optimise that spend. Also, organisations are exercising caution given the macroeconomic uncertainty.”

“Q4 saw slower growth in consumption as customers optimised GCP cost in response to the macro backdrop.”

2023 looks to be a gloomy year for enterprise IT spending. The market is focused on the short-term, and share prices have fallen as analysts pull back growth forecasts. However, long-term investors can be reassured knowing there are clearer skies ahead and thus invest opportunistically.

Cyclical/short-term headwinds

The cyclical nature of cloud spend is a positive signal. It validates the flexible and scalable nature of cloud computing. Current macro uncertainties have compelled companies to reduce their spend which clearly demonstrates the benefit of cloud’s flexible operating costs. In fact it amplifies its value in comparison to the rigid fixed costs and capacity of on-premise IT infrastructure.

As cloud users realise greater efficiency from optimisation efforts, they are able to reinvest cost savings towards transforming other workloads to the cloud. This in turn will boost cloud revenue over the long run. Additionally, cloud companies are developing services and products to provide better customer experiences. Again, this will drive larger and longer-term spending commitments from users.

Towards the second half of 2023, the optimisations will have worked their way through the system. As economic uncertainties are clarified and organisations adapt to new operating environments and customer preferences, cloud migrations will revive at pace. As more operations move to the cloud it will become increasingly business critical, which will reduce cyclical variation.

Fundamental growth drivers for the next decade

The amount a company is willing to invest is dictated by the return on investment (ROI). There are two ways to increase ROI: increase return or decrease cost.

The cloud industry is poised for growth as companies with cloud-first strategies generate outsized returns at lower costs.

Increasing returns from cloud computing investments

During the pandemic, cloud growth rocketed as economic activity shifted online and companies scaled up their digital operations. Companies valued the cost savings, scalability, improved accessibility to market-leading technology and data security that came with the cloud. These attributes are enormously valuable as businesses focus on efficiency, ultimately a function of productivity, speed and cost structure.

International Data Corporation (IDC) projects global spending for digital-transformation efforts will reach $2.8 trillion by 2025. McKinsey estimate cloud adoption can generate $3 trillion of EBITDA value for Forbes Global 2000 companies by 2030.

At Swell, we monitor companies across various industries, and we have seen one common theme … ‘do more with less’. Enterprises want to serve customers better with fewer resources, evidenced by recent tech layoffs. On the other hand, customers want better experiences with less effort. The only way to achieve both is to digitally capture complementary data. Actionable insights can then be extracted using Artificial Intelligence (AI), but this requires scale and cloud based computing.

AI needs scale

AI is top of mind currently (and at the top of stock market gains with AI-related stocks such as BigBear.ai up 467% year to date as of 15-Feb-23). I won’t dwell too much on AI here but read this great article from my colleague Alex if you are interested in companies poised to benefit from AI.

One thing is certain, AI will play an increasingly important role in our lives, becoming a huge tailwind for cloud computing growth. But AI systems critically require scale, with vast amounts of computing power, storage, data and tools.

Cloud computing enables organisations to implement AI systems and access AI capabilities that would be too costly and complex to run on-premises. Moreover, AI enhances cloud computing. It can optimise and automate various aspects of cloud computing, such as resource management, security, and operating costs.

AI advancements and demand for related cloud services will take time to materialise. The massive opportunity is unlikely to offset current headwinds in the enterprise market over the next few quarters. But it will strengthen the moat around companies with significant AI and cloud computing resources over the long run.

Cloud computing costs will continue to trend down

Both hardware and software improvements have lowered computing costs significantly. Training the GPT-3 language model that powers ChatGPT, with over 175 billion parameters, cost $4.6 million in 2020. In 2022, the same training would have cost only $450,000, equating to a 70% annual reduction. If that rate continued, the same model would cost only $30 to train in 2030. This significantly democratises access to larger and better AI systems. That, in turn, will open up substantially more use cases and improved productivity.

Training the model is merely the first step. Continuous learning and enhancements maintain its value. But this requires massive amounts of data storage and compute power, and as the population of models expands, the IT needs will increase exponentially.

In the past decade, Amazon, Google and Microsoft have efficiently allocated capital towards compute infrastructure, amassing significant capacity. Infrastructure spending in 2022 reached $700 billion, with hyperscale operators now accounting for 29% of the total, up from just 13% in 2016.

Besides infrastructure, the three public cloud providers have invested heavily in dedicated hardware for AI workloads. Amazon’s custom chips, AWS Graviton and Inferentia, target high performance compute and inference. Google has designed TPU accelerators to accelerate machine learning workloads. Microsoft has partnered with Nvidia to build AI-first supercomputers in the cloud.

These efforts will improve compute efficiency and lower compute costs.

Opportunity

The market opportunity breaks down into a simple equation:

GDP x IT spend % x Cloud computing penetration %

According to Gartner, global IT spend as a percent of GDP was 4-5% from 2012 to 2021. Most analysts predict future IT spend compared to GDP will remain at that level. However, we believe digital transformation efforts combined with exponential improvements in AI will boost IT spend as a percentage of GDP. And we expect cloud computing will take an increasing share of IT spend. In 2022, public cloud ecosystem revenue reached $544 billion or 12% of total IT spend.

Market opportunity 2030:

~$117 trillion x 6% x 36% = $2.5 trillion

* Assumptions: GDP grow at 2% annually from ~$100 trillion in 2022. IT spend as % GDP reach 6%. Cloud penetration to triple from 12%.

Amazon, Google and Microsoft held a combined 35% share of the market in 2022. Assuming they maintain market share, their combined cloud revenues would reach $875 billion by 2030. In 2022, cloud revenues at the three cloud leaders reached $188 billion (AWS: $80.1, Microsoft Intelligent Cloud $81.8, Google Cloud $31.8). This is a 365% upside, without considering each company’s other valuable revenue streams!

Enterprise computing is now entering the cloud-first era, as it has become the critical component powering end-to-end digital transformation.

About the Author